A permanent disability will change what the rest of your life looks like.

It can also make life much more expensive in terms of medical care and home modifications – which is why TPD cover is so valuable.

When you’re looking at TPD cover, there are 3 key things you need to understand so you know what you’re covered for, and what that means at claim time:

- How your claim will be assessed – Any or own occupation

- How long your claim will take – Maximum medical improvement

- How your cover is structured – Stand-alone or linked

Any or own occupation

When you start a TPD cover policy, you may be given a choice of definition that will apply at claim time. The two main choices are:

- Own occupation – Where your claim is assessed against your ability to perform the specific requirements of the job you currently do, or

- Any occupation – Where your claim is assessed against your ability to perform any job you are qualified or suited to based on your education training or experience

Say you’re a cabinet maker who permanently lose the use of one of their hands. Under an own occupation definition, you’re likely to be considered totally and permanently disabled as you’ll never be able to perform your current job again. But under an any occupation definition, you may still be able to work for a building supply company providing advice or as a TAFE teacher which means you may not be considered totally and permanently disabled.

With a greater likelihood of a claim being accepted, an own occupation definition typically adds to the cost of TPD, and it may not be available to all occupations.

Maximum medical improvement

TPD cover claims can take longer to pay than other types of life insurance, mainly because of the complexity involved in determining whether a disability is permanent.

Generally a TPD claim will only be paid when you obtain “maximum medical improvement”. That means you need to have had any operations, rehabilitation or medical procedures recommended by your treating doctors.

As you can imagine, a TPD cover claim can take months or even years to play out, and it does have a higher decline rate than other cover types because of the difficulty in proving permanency. For those reasons, TPD cover is often taken in conjunction with trauma cover – which can provide more immediate financial support for a defined list of serious medical conditions.

Linked covers

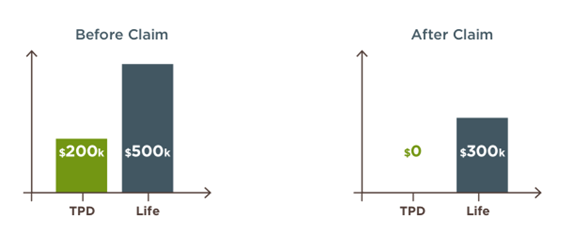

TPD cover may be purchased as a stand-alone policy or as a ‘linked policy’ that’s connected to life cover or trauma cover.

Linking policies reduces your premium, but there are major implications at claim time.

Say you have a $200,000 TPD cover policy linked to a $500,000 life cover policy. If you make a successful claim on your TPD cover, your life cover benefit will reduce by the $200,000 paid out (i.e. to $300,000).

Depending on your situation you may be eligible to buy back this extra life cover at some point, but it’s important to note that your life cover is significantly reduced in the meantime.

Did you know?

There’s a common exclusion on TPD cover policies that means you generally won’t be covered if your disability is caused by any self-inflicted act. You can find details of any exclusions in the Product Disclosure Statement (PDS).

For any Financial Services assistance, please speak to a Financial Planner now at BW Private Wealth Financial Planning | Ballarat | Ararat | Surrounds